MASUK

MASUK

DAFTAR

DAFTAR

SALDO ANDA

PROFIL SAYA

PROFIL SAYA BERANDA

BERANDA PERMAINAN

PERMAINAN Myshowtime E-Learning BERITA PROMOSI DUKUNGAN KELUAR

Myshowtime E-Learning BERITA PROMOSI DUKUNGAN KELUARJika Anda mengkonfirmasi PENDAFTARAN, berarti Anda menyetujui pernyataan privasi, syarat & ketentuan, dan perjanjian layanan 8elements kami.

Kode verifikasi telah dikirim ke ponsel Anda:

Masukkan kode verifikasi telepon di sini:

We have redirected you to your selected payment channel and they are processing your payment request. It may take some time to execute a secure payment, please be patient ..

Something went wrong. We suggest you contact the selected payment channel directly and talk to their customer service people and choose a different payment method to buy what you like and want

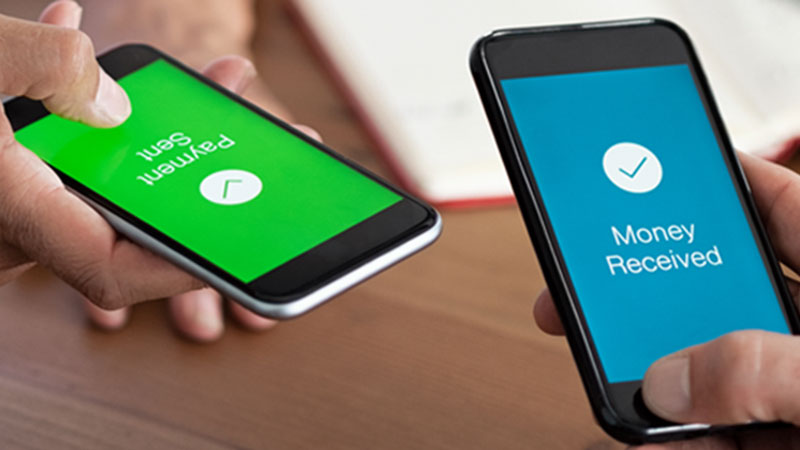

We live in an instant world. But unfortunately this does not apply in terms of payments. We still often send money to the bank but the funds will only arrive a few days later. Even that can not be done on weekends or holidays. Fortunately, now there is a technology called instant payment.

Maybe some of us have heard of instant payments, but maybe we don't know how it works. The following article will explain it, starting with the definition of instant payment itself to some examples.

DEFINITION

The European Central Bank defines instant payments as electronic retail payments that are processed in real time, 24 hours a day, 365 days a year, where fresh funds are immediately available for use by recipients within seconds.

So it boils down to the speed at which funds arrive, no matter what medium is used. We can call payment by debit card an instant payment, as well as transfers via digital wallets.

In fact, we cannot call direct remittances to banks using the RTGS method an instant payment, even though in practice the bank does all the processing electronically. Because the RTGS method usually takes several hours for the funds to reach the beneficiary's account.

Meanwhile for e-commerce, instant payment eliminates the risk of merchants not being paid or experiencing fraud. They can check directly whether the payment has arrived before releasing the item.

HOW IT WORKS

What happens behind all the processes when we use instant payments? In the process, this is roughly the explanation:

1. Initiation

When someone wants to make a payment, he must be connected to the bank where the money is kept, or through the mobile banking application, then fill in the nominal amount and the destination account number.

2. Authorization

The next instant payment stage is authorization. After submitting a payment request, the bank will ensure that the account has sufficient funds. Once confirmed, the bank will issue money from the account and send payment information to the beneficiary's account.

3. Transmission

The bank of the destination account receives payment information from the sending bank and validates it.

4. Reception

The destination bank will reconfirm with the sending bank that they have received the transaction and add the balance to the destination account.

5. Receipt

The instant payment stage is complete. The sender and recipient receive a notification from their respective banks that the payment process has been completed and the money has entered the recipient's account.

Of course the above steps are simplified processes. In practice, this would involve exchanging more complex data and would be very fast.

One thing that differentiates instant payments from conventional electronic payments is the involvement of a mediator. In instant payments, there are really only two parties involved, namely the sender and the bank (or other financial institutions such as digital wallets) as well as the recipient and the bank.

In conventional electronic payments such as RTGS, there is a mediator. In Indonesia, it is Bank Indonesia (BI). So the sending bank must go through the process to BI before being forwarded to the receiving bank. That also causes payments to take much longer.

CONCLUSION

Currently, there are many applications that allow instant payments with their respective advantages. In this way, the time required for the payment process can be reduced by up to 80 percent, because it eliminates work such as manually inputting data.

In the future, instant payments will become more and more commonplace. Therefore, whoever we are, of course, must get used to this. Even if you're doing business, instant payments implemented through payment software have many advantages.